Might even call it a black swan

March 14, 2023

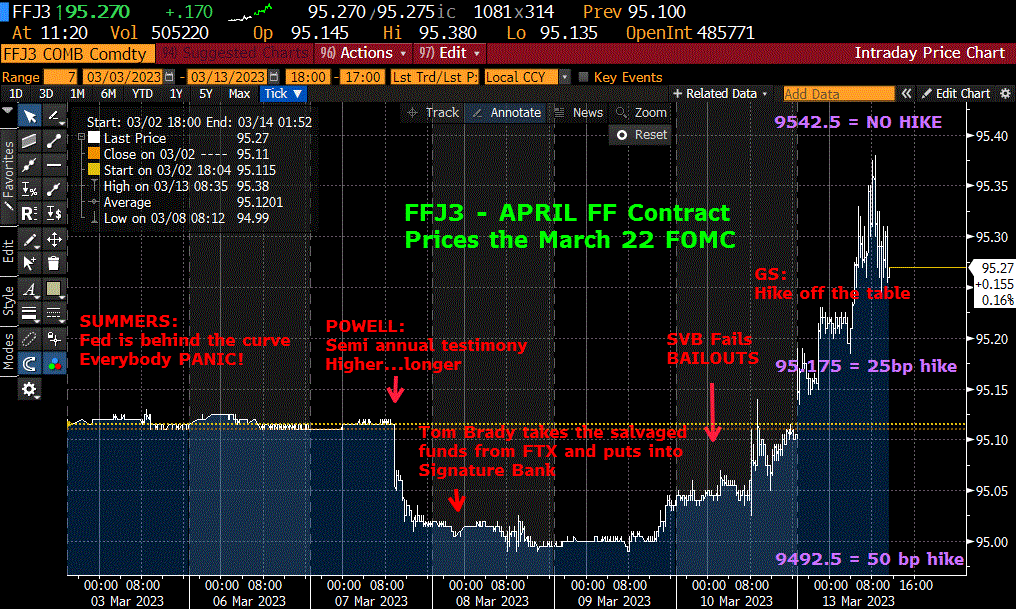

–On March 8, the low contract on the FF curve was October 2023 at 9431.5, which you might call the peak terminal rate of 5.685%. The FFU3 contract was close at 9533.0. Yesterday, FFV3 settled 9577 or 4.23%, a rally of 145.5 bps in a few sessions! Currently the low on the FF curve is FFK3 which settled 95.24 or 4.76%. In other words, peak FF has had 100 bps lopped off in a few days. Current EFFR is 4.57 or 95.43. April FF settled 9528.5 or 4.715; the difference to EFFR is 14.5 bps, so as of yesterday’s close, this contract reflects an even split between 0 and a 25 bp hike for next week’s FOMC.

–Today is, of course, CPI, expected 6.0% yoy with Core of 5.5%.

–Jim Bianco notes (twitter) “Today the 2-yr note declined 61 bps. This was the biggest one day decline since Oct 1, 1982… to emphasize, today’s decline in the 2-yr was larger than any one day seen during 2007- 2009…” Sept’23 SOFR contract settled up 101 bps at 9588.5, but had a range of 123.5. Unsurprisingly volume was massive on the SOFR curve at 14.5 million. Open interest fell slightly, with the bulk of the drop occurring in H3 at 122k (continues to trade even though IMM date has passed) and M3 which fell 72k.

–Curve had a huge move as flatteners, which had made new historic lows sparked by Powell’s semi-annual testimony last week, were exited at any cost. 2/10 was -110 on March 8 and -51 yesterday.

–SFRM3 9562.5^ settled 93.25 with futures 9658. On Thursday, SFRM3 settled 9443.5 and the 9437.5 straddle settled 34. The price of insurance is going up. Also on Thursday, FFJ3/FFJ4 spread, which can be thought of as a proxy for the Fed’s moves over that year, was POSITIVE 8.5. Yesterday it slipped to NEGATIVE 101.